The Kodak Australasia Pty Ltd Superannuation fund was one of many innovative benefits provided for staff.

The Superannuation fund was established in January 1940. This early adoption of a superannuation scheme was possibly prompted by Eastman Kodak Company, who followed the United States of America's corporate system of pension plans for their employees. The fund was implemented by a Trust Deed and administered by a group of trustees, representing both the company and the employees. The benefits were secured by The National Mutual Life Association of Australasia Limited.

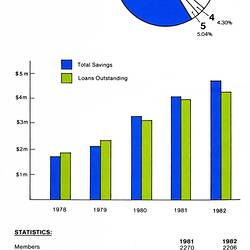

Membership in Kodak's superannuation fund was compulsory for permanent employees and began on the first day of the month following an employee's 25th birthday or after six months service with the company. Contributions were deducted from the employee's pay. The amount paid made to the fund was calculated on the basis of the salary grade of the employee and generally amounted to 4% of their salary.

Kodak Australasia Pty Ltd also contributed towards an employee's superannuation fund - this contribution was generally twice what had been contributed by an employee, based on their salary grade. Former Managing Director, John Habersberger, referred to the fund as the "cornerstone" of Kodak's employee benefits. This view is justified considering Australian employers were not required to make superannuation contributions until the 1990s when the Australian Government introduced the 'Superannuation Guarantee' as part of the 1991 budget.

The retirement pension was the principle benefit of the fund and was payable for life for a member who retired at 65 years, or at 60 years in the case of women who were members of the Fund, prior to the 1st of October 1959. The pension was calculated to ensure maximum yield, and total service with Kodak companies, irrespective of breaks in service, was taken into account. This included instances of early retirement, taken with the consent of the company, ten years prior to the normal retirement date (i.e. at 55 or 50 years).

If a member left the company before retirement or took early retirement, they would be refunded their contributions to the fund plus 3% compound interest. Former Kodak employee, Trish Lobb, remembers her benefit being a "considerable amount of money" when she left the company before retirement age. However, if the member had been working at the company for fifteen or more years they could be, at the trustee's discretion, eligible to also receive the company's contribution to their pension.

Members were able to nominate a beneficiary for the fund, either a spouse or someone else of their choosing, who could inherit their funds in the event of their death. It was not compulsory to nominate a beneficiary and it could be changed at any time.

An optional Death benefit was also available through the fund with employees contributing an extra ½ per cent of their salary. Kodak would generally contribute twice the employee's contribution towards this fund as well. In the event of a member's death before retirement, this benefit would enable their beneficiary to receive two years' salary. Members were also covered by their Death benefit, at a reduced rate, following retirement.

A Disablement benefit was available in the event of total disablement, usually considered to be the loss of limbs or eyesight. This benefit entitled a member to receive the total of their contributions to the fund paid toward their pension, a disablement benefit of approximately two years' salary and a pension for life.

Kodak purchased separate cover for death and disablement, similar to the superannuation fund, for all employees under the age of 25 years with six months service, who weren't eligible for the main Kodak scheme. Employees did not have the right to designate a beneficiary for this fund and, in the event of death or injury, moneys would be paid to a legal representative or next-of-kin.

A booklet titled 'An Outline of the Staff Superannuation Plan' was given to all staff to explain the benefits and entitlements in 'layman's terms'. Museums Victoria holds a number of examples of this booklet dating from the 1960s to 1980s. Museums Victoria's collection also includes documents with more in-depth explanations of the fund, including the indenture and rules governing the fund's administration. Some personal documentation donated by former Kodak staff relating to their superannuation also forms part of Museums Victoria's collection.

References:

'Australia's Future Tax System - Retirement Income Consultation Paper - Appendix B: A History of Superannuation', Australia's Future Tax System, at: http://taxreview.treasury.gov.au/content/consultationpaper.aspx?doc=html/publications/papers/retirement_income_consultation_paper/appendix_b.htm accessed: 30.10.2018

'Australian Kodakery', No 3, Sep 1968 (HT 35700)

'Australian Kodakery', No 58, Apr 1975 (HT 35774)

'Australian Kodakery', No 59, Jun 1975 (HT 35775)

Booklet - Kodak Australasia Pty Ltd, An Outline of The Staff Superannuation Fund, 1 Jul 1968 (HT 31101)

'Chronology of superannuation and retirement income in Australia', Parliament of Australia, at: https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Library/pubs/BN/0910/ChronSuperannuation accessed: 30.10.2018

More Information

-

Keywords

-

Authors

-

Article types